Are Tariffs Really Cooling Down Inflation? What the White House Isn’t Telling You

Series on Tariffs

The White House recently cited a Federal Reserve Bank of San Francisco working paper as evidence that tariffs don’t cause inflation.

The claim is technically accurate but “forgets” to include critical context about how this effect actually works. The paper is actually much more damaging to the Trump administration’s trade policy agenda than they may realize. Let’s jump into the paper and the data!

What the Fed Paper Actually Found

The paper “What Is a Tariff Shock? Insights from 150 Years of Tariff Policy” by Régis Barnichon and Aayush Singh analyzed 150 years of U.S. tariff data (1870-2020), plus additional data from France and the UK during the first wave of globalization (1850-1913).

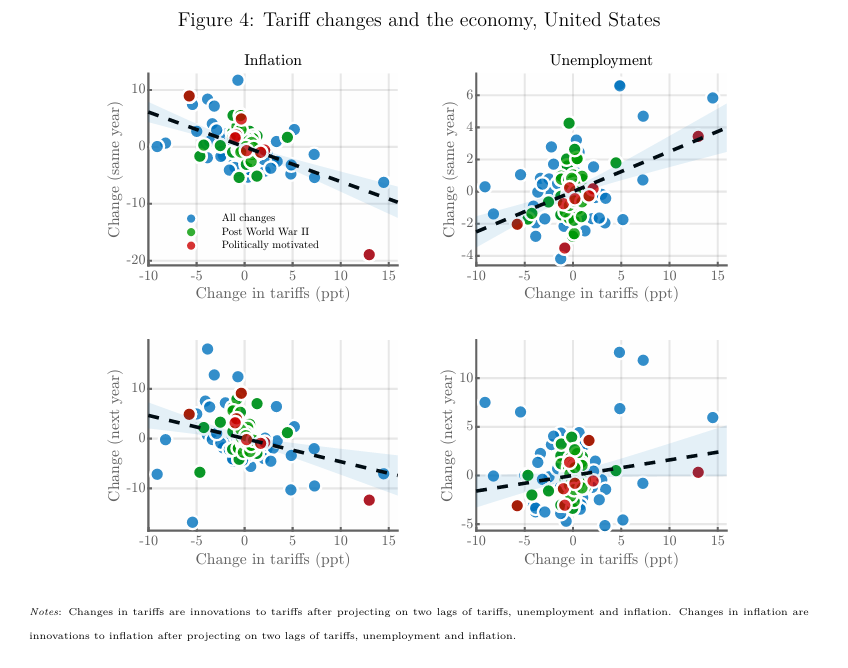

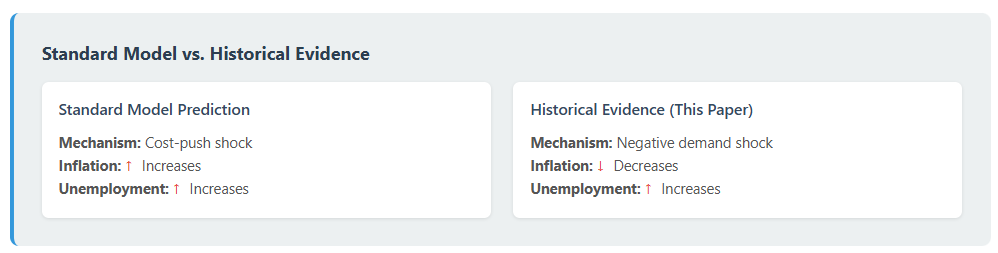

The researchers found that when tariffs increased, inflation decreased in the short run rather than increased as standard economic models predict. However, this happened because tariffs acted as “negative demand shocks”, they raised unemployment and contracted economic activity.

The mechanism: tariffs lowered inflation by damaging the economy, not by improving it.

Scale Matters: Large vs. Marginal Changes

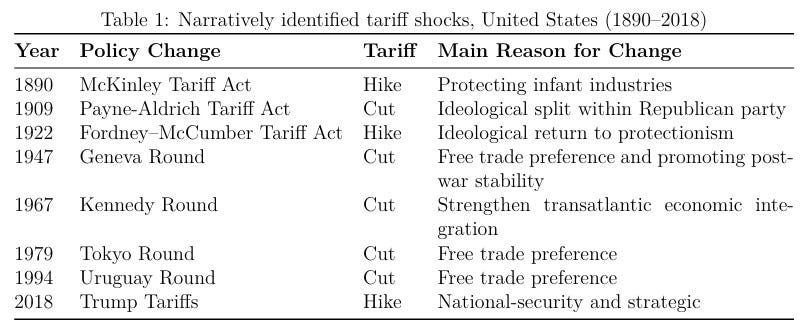

This paper looks at large tariff changes, not marginal adjustments. The researchers studied episodes where tariff rates jumped 5, 10, or even 20 percentage points in a single year.

Historical examples:

McKinley Tariff (1890): raised average tariffs to nearly 50%

Smoot-Hawley Act (1930): pushed tariffs to 59%, the highest in U.S. peacetime history

First wave of globalization (1870-1913): rates occasionally rose or fell by 10-20 percentage points annually

The paper notes: “Between the end of World War II and 2025, yearly tariff changes were very modest, orders of magnitude smaller than the 15 percent increase in average U.S. tariffs in 2025”.

For small, marginal tariff adjustments (0.5-1 percentage point), the standard economic relationship likely holds: modest price increases with minimal economic disruption. But large tariff increases trigger different dynamics. They create significant economic uncertainty that depresses confidence and spending, producing negative demand shocks.

The 2025 tariff increase is “unprecedented in the modern era”. To find comparable increases, you must look back to the historical periods this paper studies. The 2025 tariffs are not marginal adjustments, they’re large-scale policy shifts where the historical patterns documented in this research apply directly.

The Empirical Results

Pre-World War II (1869-1939):

A 4 percentage point tariff increase lowered inflation by 2 percentage points on impact

The same increase raised unemployment by approximately 1 percentage point

Post-World War II (1946-2020):

Estimates are less certain due to much smaller tariff variations, but the pattern holds: higher tariffs led to lower inflation and higher unemployment

International Evidence: Analysis of France and UK data (1850-1913) produced consistent results: tariff increases lowered inflation and contracted economic activity

The researchers used two identification strategies:

Narrative identification: isolating tariff changes explicitly motivated by long-run considerations rather than business cycle conditions

OLS estimation: exploiting the quasi-random nature of tariff changes due to opposing partisan views on tariff policy

Both methods produced similar results, strengthening confidence in the findings.

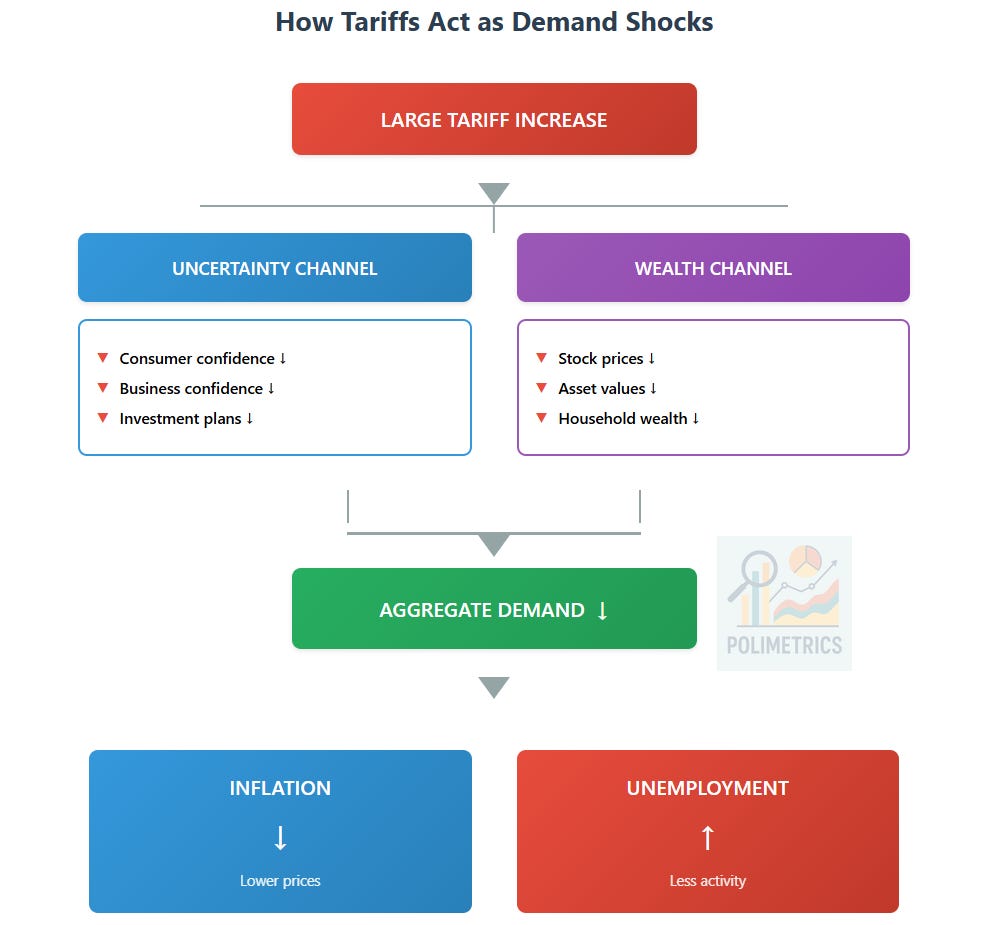

How Large Tariff Increases Work

The paper provides evidence for two transmission mechanisms. First, tariff shocks create economic uncertainty that depresses consumer and business confidence, reducing spending and investment. Second, tariffs trigger declines in asset prices, which reduce wealth and further dampen aggregate demand.

The researchers found that in response to higher tariffs, stock prices declined and stock market volatility increased, supporting both proposed channels.

This explains why large tariff increases act as aggregate demand shocks rather than the cost-push shocks predicted by standard models. The uncertainty effects dominate the direct price effects when changes are large enough.

Policy Implications

The Federal Reserve must understand whether tariffs are inflationary (requiring tighter monetary policy) or deflationary through demand destruction (requiring looser monetary policy). The paper’s findings suggest large tariff increases fall in the latter category.

For policymakers considering tariff policy, the trade-offs are clear:

Large tariff increases may reduce inflation

But they achieve this by raising unemployment and contracting GDP

The effect operates through increased economic uncertainty and lower consumer confidence

This is not a favorable policy trade-off. It replaces one economic problem (inflation) with others (unemployment, slower growth, increased uncertainty). One could argue that perhaps achieving the policy objective the Trump admin is trying to produce would outweigh the negative impacts, but it really is not clear what that policy objective is for this administration.

The Selective Citation Problem

The White House cited this paper to argue tariffs don’t cause inflation while omitting that:

The paper studies large tariff changes comparable to 2025 levels

These changes raise unemployment

They lower economic activity and GDP growth

They reduce stock prices and increase market volatility

All of these findings appear in the same paper being cited as evidence that tariffs are benign for inflation.

Coming Up Next: Testing the Theory with Real-Time Data

The Fed paper shows that historically, tariffs acted as negative demand shocks, reducing consumer and business spending, which then lowered both inflation and economic activity. But are we seeing this pattern play out with the 2025 tariffs?

In the next post, we’ll examine real-time data on aggregate demand to answer this question. Specifically, we’ll track:

Consumer Confidence Indices: The University of Michigan Consumer Sentiment Index and the Conference Board Consumer Confidence Index, which measure how households view current and future economic conditions

Personal Consumption Expenditures: Monthly data on actual consumer spending across goods and services categories

If the historical pattern holds, we should see declining consumer confidence and reduced spending growth following the tariff implementation. If we don’t see these effects, it would suggest something different is happening this time, perhaps due to changes in the structure of the modern economy, different monetary policy responses, or other factors.

We’ll also compare the magnitude of any observed effects to what the historical relationship would predict, helping us understand whether 2025 is following the script or writing a new chapter.

Stay tuned for the data.

Sources:

Barnichon, Régis and Aayush Singh. 2025. “What Is a Tariff Shock? Insights from 150 years of Tariff Policy.” Federal Reserve Bank of San Francisco Working Paper 2025-26. https://www.frbsf.org/wp-content/uploads/wp2025-26.pdf

Couldn't agree more. It's classic garbage in, garbage out when you cherry-pick data. Thanks for this insightful analise!

Thanks again for sharing and synthesizing data that makes esne and needs minding.

The "conclusion" drawn by the administration is as incorrect, cherry-picked, and self-serving as all the other instances they've tried to pass off a pseudoscientific confirmation that they both have a plan, and that it's working.

It's not.

It's also the same tired economic theory that's been disproven over and over - that's of trickle-down economics.

Modern Monetary Theory (MMT - which is the more accepted model that economists are trying to move governments towards utilizing) works because it starts from the Keynesian premise that governments role is NOT to get out of the way of profit seeking. It is instead meant to use their fiat currency to set priorities that best promote stable, healthy conditions with the money it creates.

Once that money is activated through loans, purchasing, creating / manufacturing, and caring for its populace and businesses it is clawed back through taxes where it is effectively "destroyed."

It recognizes that money isn't the objective - it's the tool that sets the floor for society to operate under.

The rentier-dominated system most countries use that is now in crisis is incompatible with that model, because a rentier dominated system is about absolute consumption.

In MMT some inflation is inevitable and reasonable. Expected. Lower inflation allows for some increase in investment, hiring, and purchasing. When there's any external shock to MMT the answer isn't austerity - it's actually investment in society to adjust for that shock.

It is also completely antithetical to classical economic theory and the abomination that is the Laffer Curve.

Where classical economic theory and trickle down economics fails repeatedly, rapidly, and with increasing frequency is that it creates a fantasy world where there's somehow and attainable growth curve represented as a mythically perfect 45% upward slope. Where the market dictates all, the government is just a roadblock or a thing to be killed, and infinite consumption and control is possible.

Trump is creating a financially critical self-inflicted wound on the US by attempting to solve a problem he doesn't comprehend, with and incorrect implementation of a financial mechanism he doesn't understand in either purpose or execution, with all the subtlety and nuance of an anvil dropped on a cartoon coyote.

Others see it. It has escaped the notice of many, but within a 72-hour timeframe 3 things have happened in the financial world that should give everybody who follows the market the heebie-jeebies.

Warren Buffet announced his retirement 4 days ago.

That same day, Dr Michael Burry closed a $2.1B hedge fund and returned the remaining money to the investors.

Both cited market activity that does not correlate to what is showing up in DJIA and NASDAQ stock evaluations.

3 days later on Sunday afternoon, mega investor and millinarian billionaire doomsday prepper Peter Thiel dumped ALL of his Nvidia stock.