Property Is Power

The Real Estate of Religious Power

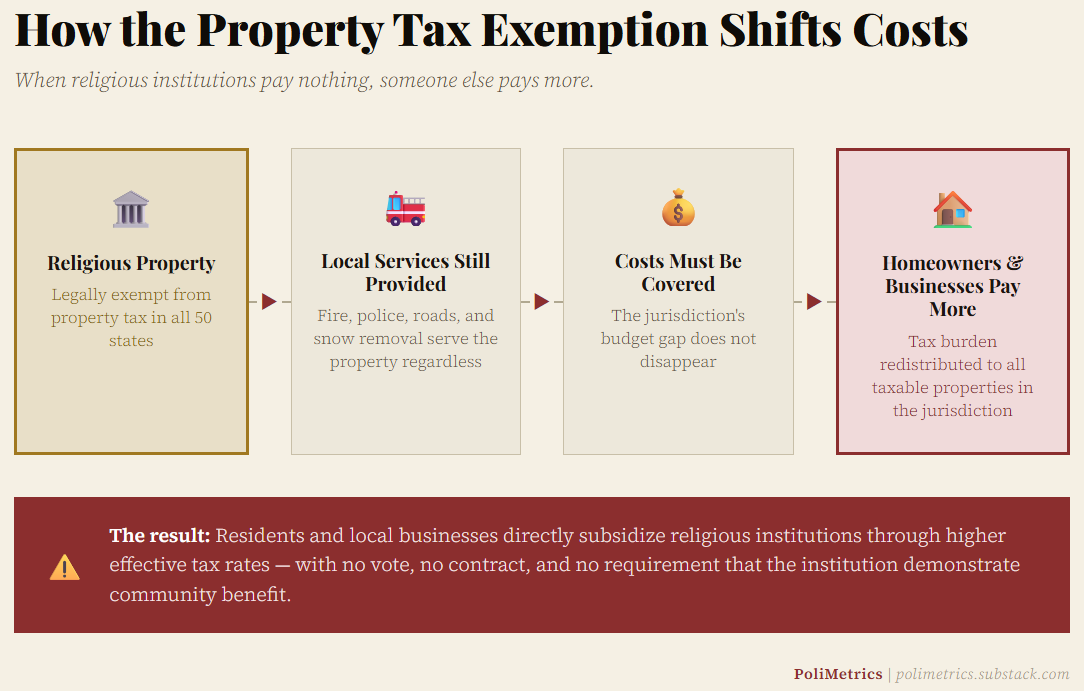

Property tax exemption for religious institutions is one of the oldest and least examined subsidies in American public finance. It exists in all 50 states. It is rarely debated. And almost nobody tracks what it actually does to the communities that absorb it.

My research tries to.

The Policy Premise

The justification for religious property tax exemption rests on what legal scholars call the quid pro quo theory. Religious and charitable institutions provide public benefits, so they deserve a public subsidy in the form of tax relief. The community gets services and social value. The institution gets to keep the tax revenue it would otherwise owe.

That seems reasonable on its face. But it assumes two things: first, that the institution actually provides benefits to the local community, and second, that those benefits are distributed to the people who bear the cost of the exemption.

Local taxpayers and local governments bear that cost directly. When a tax-exempt parcel sits in a jurisdiction, the jurisdiction still has to provide police protection, fire service, street maintenance, and other public goods. Those costs get shifted onto homeowners and businesses that are not exempt. The Lincoln Institute of Land Policy estimates that local governments forgo 4 to 8 percent of total property tax revenues annually because of nonprofit exemptions. That is not a rounding error.

The question worth asking is whether the benefits flow back to the same people absorbing that cost. My research suggests that at least in some cases, they do not.

What the Evidence Shows

I did an empirical analysis on the fiscal and demographic effects of Mormon temple dedications using a quasi-experimental research design. Mormon temples are useful for this kind of analysis because their locations are deliberate institutional decisions, their dedication dates are known in advance, and their physical presence is permanent and substantial. They are, in research terms, a clean treatment.

The findings are consistent across the panel. After a temple is dedicated, surrounding neighborhoods experience increases in median household income, educational attainment, and homeownership rates. Property values rise. The tax base expands.

That sounds like a net positive until you look at what happens to poverty rates. They do not improve. They displace.

Lower-income residents move out. Higher-income residents move in. The neighborhood composition changes in ways that benefit wealthier, more educated households while pushing working families further from economic opportunity. The institution anchors in place. The community around it reorganizes around the institution’s presence.

This is not speculation. It is a measurable, replicable pattern across multiple temple dedications over time.

The Mechanism Nobody Talks About

Property tax exemption removes a major fiscal constraint from religious real estate development. An institution that does not pay property taxes can acquire and develop land without the financial pressure that shapes decisions for every other landowner. It can hold large parcels in high-cost areas indefinitely. It can develop on a timeline driven by institutional strategy rather than market pressure.

That advantage compounds over time. Churches hold billions in real estate assets. Those assets generate no property tax revenue for the jurisdictions that surround them, even as those jurisdictions provide fire protection, police patrols, and road maintenance to the properties.

When a well-resourced institution develops a major facility in a neighborhood, it changes who finds that neighborhood desirable. It signals stability, investment, and a particular social environment. That signal attracts some people and, through housing market pressure, displaces others.

The institution contributes nothing to the fiscal cost of managing that displacement. The local government absorbs it without any mechanism to recover revenue or negotiate compensation.

Why This Matters Beyond Mormonism

This post uses Mormon temples as the empirical case because that is where the research is. That’s the context I know best. The quasi-experimental design requires a specific, measurable institutional event with a known date. Temple dedications fit that requirement. They are not unique in their dynamics.

Catholic dioceses hold substantial tax-exempt real estate portfolios in urban markets across the country. Evangelical megachurch networks are expanding their physical footprints into suburban and exurban communities with the same tax advantages. Jewish institutions, historically Black churches, and many other religious organizations benefit from the same exemption structure.

The pattern my research identifies is not a Mormon problem. It is a policy problem. Mormonism is the clearest available case study for what that policy produces at scale.

Those exemptions impact local communities in ways that haven’t really been studied much with data. I want to understand better what we’ve maybe taken for granted, and maybe discover a few ways to improve our system of governance that helps make our communities stronger for everyone, religious or not.

The Connection to Institutional Power

Christian nationalism is often analyzed as a cultural or rhetorical phenomenon. Researchers focus on political rhetoric, electoral behavior, and the ideological content of religious messaging. That work matters. But it points to a question that rarely gets asked: how does ideological influence translate into durable institutional power?

The answer is usually infrastructure. Legal infrastructure. Financial infrastructure. Real estate infrastructure. Rhetoric moves people; property holds ground.

Tax exemption is part of that infrastructure, and not a small part. It allows religious institutions to accumulate property at scale without the fiscal accountability that applies to every other major landowner. It enables the kind of demographic reshaping my research documents. And it does all of this without any requirement that the institution demonstrate local community benefit, disclose financial activity, or submit to democratic oversight.

That is true regardless of which institution benefits, be it evangelical megachurches, Catholic dioceses, LDS temples, or any other tradition. The structure itself concentrates power and insulates it from accountability. Whether any particular institution uses that advantage well or poorly is a separate question. The policy architecture deserves scrutiny independent of the answer.

What Comes Next

This post sets up a research agenda that I hope to pursue, trying to understand how religious institutions interact with tax policy, municipal finance, and local-level public welfare. Future posts will look at specific cases, model what a fair payment in lieu of taxes (PILOT) might look like for major religious developments, and examine the broader question of what the public actually gets in exchange for the exemptions it provides.

The goal is not to argue that religious institutions should lose their tax-exempt status. The goal is to apply the same empirical scrutiny to religious institutional behavior that we apply to corporations, government agencies, and other powerful actors.